.avif)

I just crossed my seventh year as a professional asset manager in the digital asset space. In TradFi, that’s still young. In crypto, it’s borderline prehistoric. With time, I’ve shifted from chasing short-term waves to studying long-term tides—and this series has been my attempt to chart them in real time.

This sixth installment continues a thesis I began two years ago, when the groundwork for the next major cycle was quietly being laid, yet invisible to most.

Since then, we’ve correctly anticipated the ETF approval, Trump’s pro-crypto presidency, the rate cut pivot, renewed crypto M&A, the stablecoin trade, and the Q1–Q2 narrative vacuum that shook out tourists before the real move began.

On April 9th, during our bi-weekly Frontier Forum, we flagged “Trump’s Liberation Day” as a critical inflection point—calling the market bottom at peak panic.

This isn’t about chest-thumping. It’s about context. This will likely be my only write-up for the next 3–6 months. And unlike the past few, this one carries urgency. I believe we’re entering the phase where positioning matters most—where the asymmetry is highest and attention is still misallocated.

Most will read this in hindsight, when the headlines have caught up. But if you’ve been waiting for a signal—this is it.

It’s time to be bullish.

Near-Term Catalysts - Signals in the Static

There are reasons I’m more bullish on blockchain technology today than perhaps at any point in 2022-24. But before diving into the longer-term, more philosophical drivers behind this cycle, we need to examine the source of immediate urgency behind this piece.

Digital asset investors have a tendency to misread inflection points. They’re cautious when the market has stabilized and is preparing to accelerate, yet euphoric when it’s already gone vertical. Today, we are in the former—consolidated, coiled, and underpriced.

Just look at the total crypto market cap excluding Bitcoin. After five years of chop, it's quietly grinding toward all-time highs. BTC, when priced in gold, is nearing a five-year peak. And while $120K may sound high to bystanders, that’s less than a 2x from 2021 levels. ETH is still down over 30% from its ATH. A recovery to the $3Ks is nothing to write home about. These are not “late-stage” prices—they’re forming the base for the next major leg up.

The winning Layer 1s will be trillion-dollar assets. Today, Ethereum sits just above $400B. Solana, the next in line, barely broke $100B. Meanwhile, Mira Murati just raised a $12B Seed Round—pre-product, pre-revenue. For once, AI is the bubble, not crypto.

So who and what will drive prices higher? Let’s dig in:

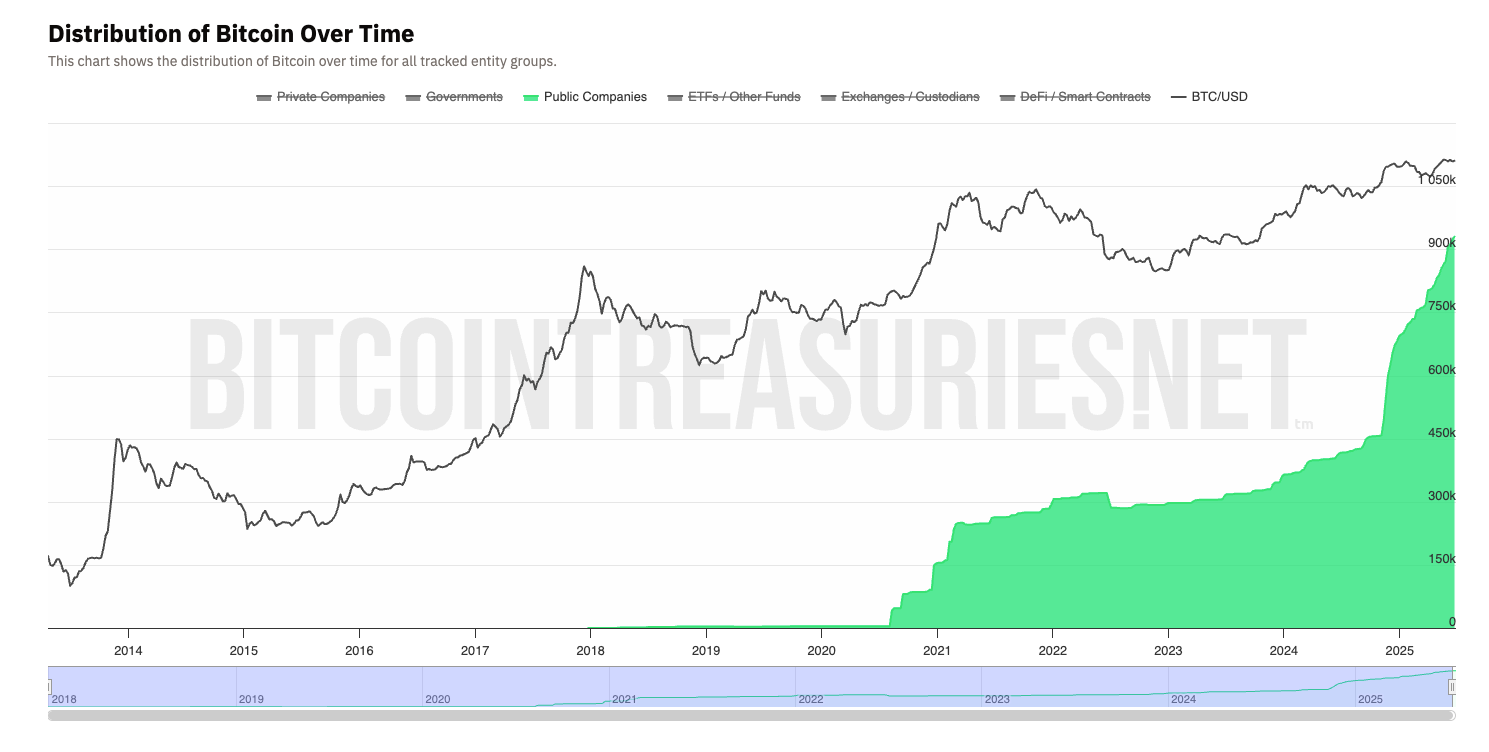

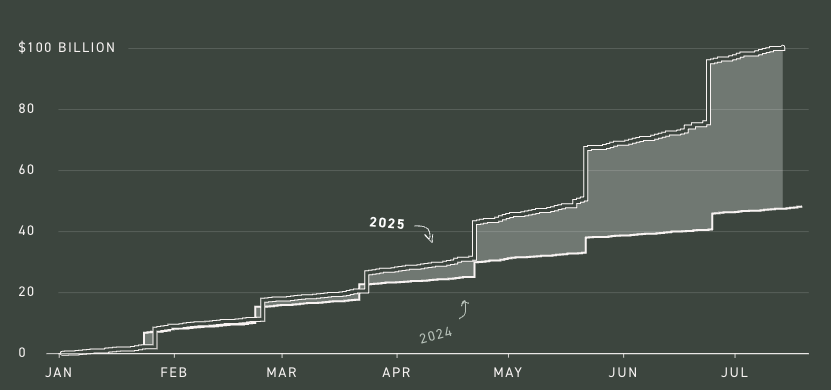

ICO 2.0 – Wall Street Style: The Rise of Treasury Companies

Michael Saylor’s “Bitcoin treasury company” playbook is gradually becoming a template.

Saylor’s pivot was born out of a dilemma: his business was stable, but stagnant, and tech giants were poaching his best talent. Sitting on $500M in idle cash as the Fed slashed rates to zero, he made a call—convert the entire balance sheet to Bitcoin. What followed was the most aggressive balance sheet expansion in corporate history: a $1B software company morphing into a $126B Bitcoin vault, now holding ~3% of BTC’s supply. (For context, his recent interview with Jordan Peterson is worth a listen if you want to understand Saylor’s life story and philosophy.)

“MicroStrategy may one day trigger the next bear market, but first, it could become the largest company in the world… Saylor will be put on par with Musk, Zuckerberg, and Huang… I believe an unraveling is inevitable, but for now, he’s sitting on tens of billions in dry powder, likely enough to push Bitcoin past $100k and unlock the next $100 billion in firepower…at least a dozen publicly traded companies are likely to adopt Saylor’s model in the next 24 months. Momentum begets momentum.”

We’re living Act II of that thesis.

But I underestimated how quickly others would follow. We're not talking about a dozen copycats in two years—we're already there.

Since then, we’ve seen high-profile launches like:

- XXI, led by Jack Mallers

- ProCap, founded by Anthony Pompliano

- Bitcoin Standard Treasury, helmed by Adam Back

More importantly, the playbook is expanding beyond Bitcoin:

- BitMine, led by Tom Lee, is an ETH treasury vehicle

- SBET, run by ETH co-founder Joe Lubin, holds ~$1B in ETH—making it the largest ETH treasury company to date

And it's not stopping there. Expect vehicles for Solana, Hyperliquid, XRP, and others. Equity-wrapped token exposure is a regulatory arbitrage—giving Wall Street the volatility it craves while satisfying restrictive mandates.

Traditional tech firms are also continuing to adopt Bitcoin as a treasury asset. Figma, in its S-1, disclosed $70M in BTC holdings and plans to acquire $30M more. Tesla, too, holds over $1bn worth of BTC.

We’re in the fourth inning of the treasury company era. Momentum is building, but for now, it’s mostly been led by high-profile insiders and figureheads. Only a handful of forward-thinking tech firms have followed suit by adding BTC to their balance sheets.

That will change fast.

Within 12 months, I expect treasury wrappers to emerge for nearly every asset in the top 10–20, alongside thematic vehicles—DeFi, DePIN, you name it. Just as ETFs multiplied once the first Bitcoin fund broke through, this structure will be replicated across the board.

More importantly, the number of publicly traded companies holding Bitcoin will likely 10x—from ~100 today to over 1,000 within two years. In an environment where artificially low interest rates no longer offset dollar devaluation, Bitcoin will increasingly be seen as prudent diversification, not speculation.

And once these flows begin, they don't reverse easily.

These entities are built to buy and hold. Selling breaks the mandate. Which means flows will be one-directional—funded by convertible debt, ATM offerings, or internal capital—but rarely unwound.

Outflows only happen in three scenarios:

- The company defaults on its notes

- Shares trade below NAV, and management chooses to unwind (unlikely for the large players)

- Shareholder activism forces in-kind distributions or asset sales

Until then, these vehicles function as black holes—soaking up scarce assets, never letting them out. The longer it continues, the tighter the float becomes. At some point, that ends in a supply squeeze.

This might be one of the easiest times in history to be long crypto.

And yet, most investors are still dramatically underweight. Why? Because they think this is all just a reflexive Ponzi—treasury wrappers, MSTR mania, too much froth.

But the real story is much bigger than Bitcoin ETFs or treasury companies. It’s the quiet rewiring of the global financial system.

Tokenize Everything - The World Goes On-Chain

It’s easy to dismiss the treasury company meta as financial theater—Bitcoin-maxi cosplay with balance sheet leverage. But that cynicism misses the deeper truth: blockchain is finally being used for what it was built to do—upgrade the world’s financial infrastructure.

The real opportunity is tokenization. Not just of crypto-native assets—but of everything: cash, stocks, bonds, treasuries, real estate, art. All of it.

I’ve said this for years, but now the world’s most powerful asset managers are echoing the same thesis. BlackRock CEO Larry Fink put it plainly in his 2025 Chairman’s Letter:

Every stock, every bond, every fund—every asset—can be tokenized. If they are, it will revolutionize investing. Markets wouldn't need to close. Transactions that currently take days would clear in seconds. And billions of dollars currently immobilized by settlement delays could be reinvested immediately back into the economy, generating more growth.

Perhaps most importantly, tokenization makes investing much more democratic.

- Larry Fink, CEO of BlackRock in Annual Chairman Letter

And he’s not alone. SEC Commissioner Paul Atkins put it even more bluntly:

“If it can be tokenized, it will be tokenized.”

- SEC Chairman Paul Atkins

We’re not talking about a fringe use case. We’re talking about tens if not hundreds of trillions of dollars in value migrating on-chain. Every tokenized asset will generate on-chain activity—and that activity flows directly into protocol revenue:

- Each transaction = fees to the underlying blockchain

- Lending tokenized assets = revenue for protocols like Aave, Maple

- Trading tokenized assets = revenue for exchanges like Uniswap, Aero, Raydium

As tokenized assets flow through the system, value accrues at every stage—settlement, lending, trading.

Just step back. The stakes are bigger than you think.

- Bitcoin may 10x from here—reaching parity with gold

- The winning Layer 1s may 50–100x—reaching parity with the GDPs of nations.

- The top DeFi protocols? They may 250x—surpassing the likes of JPMorgan

Crypto’s addressable market just expanded by orders of magnitude. The narrative is no longer about whether blockchains have utility—it’s about how much value they can settle, store, and monetize. The shift becomes even more compelling as we move beyond wrapping legacy equities and begin seeing startups launch as tokenized entities from day one. Public digital asset markets would then quickly become the new venue for discovering emerging talent—with liquidity built in from inception.

A narrow set of assets powers this entire stack—and they now stand among the most asymmetric risk-reward opportunities in global public markets.

All Roads Lead to Devaluation – Rates, Debt, and Failed Austerity

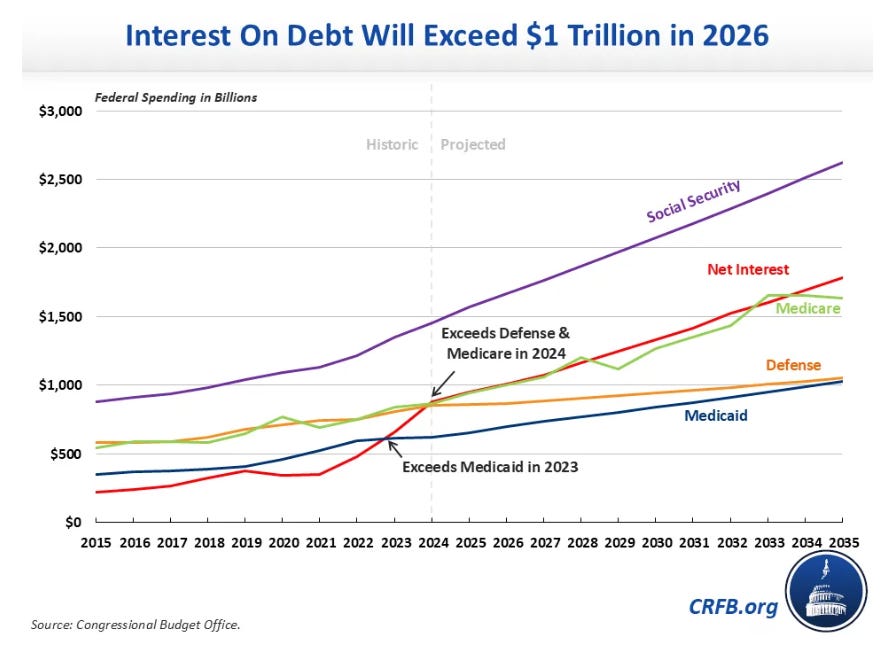

Bitcoiners have long warned of dollar debasement and fiscal irresponsibility enabled by fiat-driven monetary policy. Now, the debt bubble they pointed to has finally entered mainstream discourse—yet there’s still no appetite to do much about it.

How do you solve a debt crisis? Step one: end the deficit. And how do you end the deficit?

A. Austerity: spend less

B. Raise revenues: tax more (through taxes or tariffs)

C. Default or restructure debt

D. Print money and monetize the debt (devalue the currency)

The Trump administration came in guns blazing, promising to confront the problem head-on. DOGE, under Elon Musk’s guidance, was meant to deliver $1 trillion in annual savings via austerity repackaged as “government efficiency.” Howard Lutnick was tasked with generating another $1 trillion annually via tariffs.

Fast forward six months: DOGE has saved just $190 billion (less than $90 billion itemized), and Elon has exited in a highly public, explosive fashion. If Elon can’t succeed with austerity—backed by a public mandate and political cover—then no one will. That takes the first lever off the table.

Meanwhile, the "Big Beautiful Bill" has added an estimated $2.4 trillion to the deficit over the next decade, while also extending tax cuts, further reducing revenue. Lever two looks equally untouchable under a Republican administration. (As a capitalist, I detest taxes as much as the next person—but when the nation is speeding toward a fiscal wall, this isn’t the time to cut revenue.) Tariffs have doubled under Trump, but still only brought in around $100 billion in seven months.

It's too little, too late.

We're not going to save our way out. We're not going to earn our way out—not unless the economy enters a sustained boom that radically expands the taxable base. And as the global reserve currency, default is unlikely. Trust in that status is worth more than suffering moderate inflation via debt monetization.

It doesn’t take a rocket scientist to see where this leads (no Elon pun intended): quantitative easing and dollar devaluation. Lowering interest rates would reduce the government’s annual interest expense—we’re already paying close to $1 trillion just to service the interest on the debt. Looser policy could also stimulate growth, broadening the taxable base without raising tax rates.

But in this environment, cutting rates won’t attract sufficient demand for Treasuries—especially with inflation expectations still elevated. To keep yields from spiking, the Fed would need to step in as a major buyer, effectively monetizing the debt. That dynamic puts downward pressure on real yields, stokes further inflation, and undermines confidence in long-duration U.S. debt. If sustained, it risks accelerating the erosion of dollar reserve status.

This is exactly the fault line between Fed Chair Jerome Powell and President Trump. Powell—who famously underestimated inflation as transitory in 2020—has since evolved into one of the few true statesmen in American public life. In a political landscape obsessed with optics and short-term wins, he’s governed with principle and long-term thinking, even in the face of likely dismissal. He remains committed to the Fed’s dual mandate, knowing full well that the consequences of monetary irresponsibility may not show up until after he’s gone. Yet he continues to do what is unpopular, but likely right.

Trump, by contrast, approaches the world like a founder: win today, dominate the moment, and deal with tomorrow once you’re holding better cards. He’s pushing for a full 300 basis point cut—down to 1%—a crisis-era move last seen during COVID, and one that has historically sent both markets and the economy into overdrive.

It might work. If so, it will go down as a defiant reset of American dominance. Or it might mark the beginning of the end, with the U.S. fast-tracking itself out of reserve currency status and exposing critical social and defense systems due to fiscal collapse.

Either way, the conclusion is the same: in 2–3 years, few rational actors will want to hold bonds or cash. The rotation into risk assets—especially the foundational infrastructure of the new financial era—is already underway.

In my view, 2025 is the year to be net short USD—particularly when so many assets outside the Magnificent 7 and Bitcoin are still trading below prior all-time highs.

The Machine Economy - Scarcity in the Age of Abundance

When I’m not wearing the hat of a hedge fund manager, I wear that of a venture capitalist. Over the past three years, I’ve backed more than 30 startups across AI, XR, and frontier tech. And every now and then, a belief begins as fringe—tinfoil even—but over time, it hardens into conviction. This is one of them.

Let’s run a thought experiment.

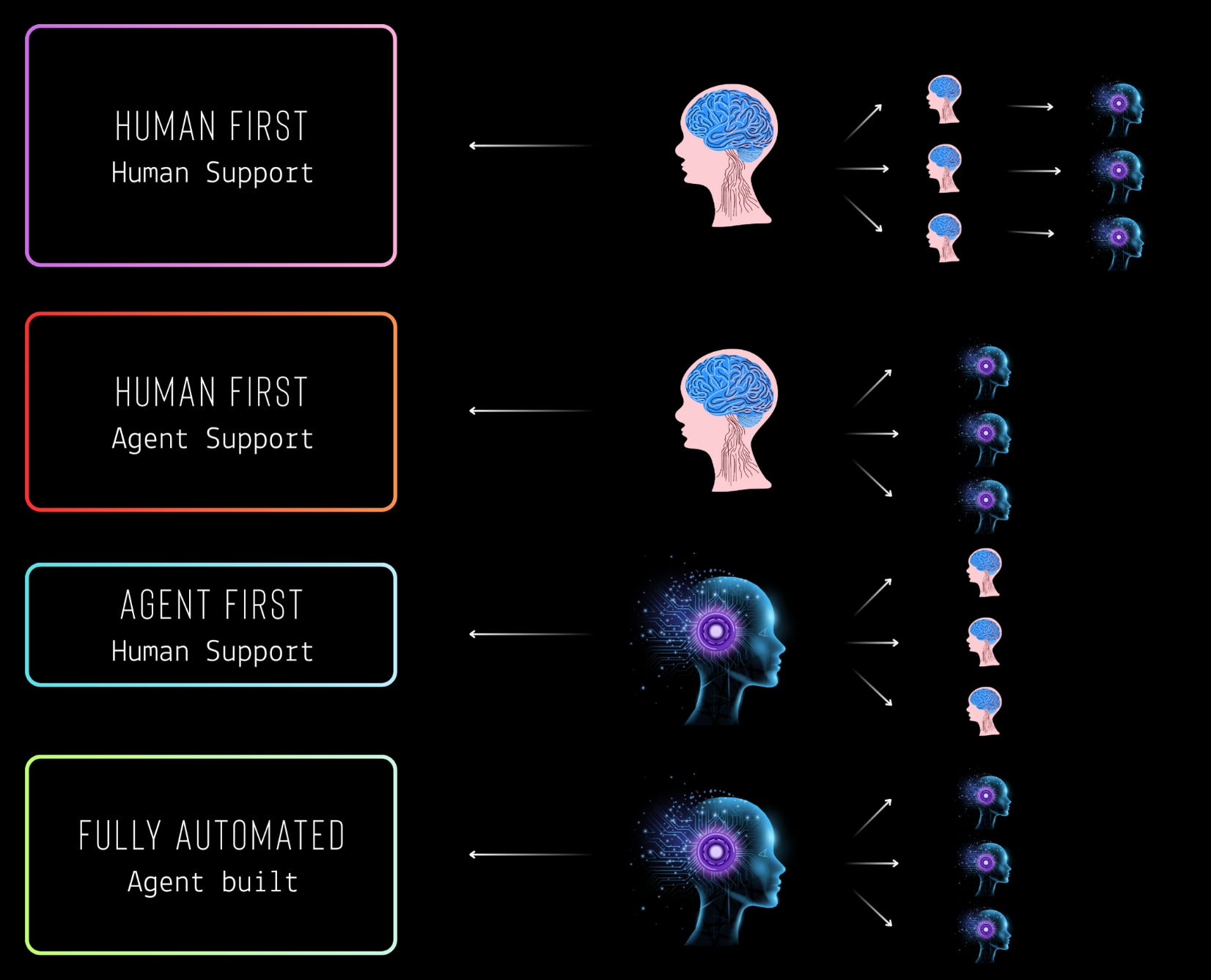

An entrepreneur starts with a team of five. With the right AI tools, that team gains the output of ten. Productivity doubles. The company begins to outcompete peers, expand margins, and grow. When it's time to build a marketing department, the founder instead deploys an AI agent with a clear mandate and KPI. The agent manages a human team, driving strategy and delegation. The humans execute, supported by additional AI tools.

As the structure scales, the founder introduces more agents—specialized ones for advertising, copywriting, outreach. Over time, the company operates with an increasingly autonomous hierarchy. Eventually, the founder asks the obvious question: why not install a CEO agent? Why not build a board of agents tasked with tuning its mandate?

Eventually, the founder steps away altogether—still the beneficiary, but no longer involved.

Meanwhile, the cost of goods and services globally has collapsed. Supply is abundant. Competition is brutal. Efficiency is the only moat—and it's being optimized into oblivion.

In that world of infinite, hyper-personalized, low-cost everything—what retains value?

You might say things. But we’re already engineering superior materials in labs. Lab-grown meat is real (for better or worse). Lab-grown diamonds are indistinguishable. You might say gold—but 2025 marks the first year asteroid mining became commercially viable. Scarcity is melting.

You might say energy. But fusion breakthroughs and microreactors suggest even that’s on its way to becoming abundant.

And so, paradoxically, in a world of boundless digital abundance, the most valuable asset may be the one with hard coded scarcity: Bitcoin. A finite denominator in a world where everything else is trending toward infinite. Most analysts get it backwards. They fixate on demand—who’s the next buyer—when the real story is supply. Bitcoin doesn’t need demand to grow in value. It needs time. Everything else inflates. Bitcoin doesn’t.

Absent a superintelligence that runs this experiment to its extreme—where all goods and services are delivered by a single entity, a dystopian outcome that could be checked by antitrust crackdowns or competition amongst ASI—we’re far more likely to see millions of autonomous, non-human agents participating in the global economy on our behalf. These agents will need to transact value, access leverage, exchange assets, and settle payments—instantly, securely, and without centralized gatekeepers.

The only infrastructure capable of supporting that at scale today is public blockchains.

As economic velocity increases, the largest beneficiaries won’t be the applications or interfaces—it will be the networks themselves. The base layers and rails that can handle agent-to-agent economic coordination in a globally secure, trustless way. In a world where businesses are run by agents, execution will be pushed to its limits. No traditional system—wrapped in bureaucracy and compliance—will be able to keep up. Banks defend themselves with paperwork. Blockchains defend themselves with code.

And code scales.

Blockchains are the only infrastructure built to meet the demands of an agent-driven economy.

Once that becomes clear, assets like Bitcoin—and leading Layer 1 blockchains like Ethereum, Solana, and Hyperliquid—alongside decade-tested DeFi protocols like Aave and Uniswap—start to look absurdly cheap.

You may not see it today. But I suspect you’ll come back to this write-up a few years from now and realize how early we were. None of this negates the volatility along the way. But I’ll repeat the same advice I have given myself over the years: stop chasing waves—study the tide. From what I can see, the flood is near.

In 2019, I thought I was late—that the real upside in crypto had already passed. In 2025, I realize everything until now was just the prelude to what’s coming.

Disclaimers:

This is not an offering. This is not financial advice. Always do your own research. This is not a recommendation to invest in any asset or security.

Past performance is not a guarantee of future performance. Investing in digital assets is risky and you have the potential to lose all of your investment.

Our discussion may include predictions, estimates or other information that might be considered forward-looking. While these forward-looking statements represent our current judgment on what the future holds, they are subject to risks and uncertainties that could cause actual results to differ materially. You are cautioned not to place undue reliance on these forward-looking statements, which reflect our opinions only as of the date of this presentation. Please keep in mind that we are not obligating ourselves to revise or publicly release the results of any revision to these forward-looking statements in light of new information or future events.

July 22, 2025

Share